24小时DY业务自助下单,在线平台真的那么神奇吗?

Efficiency in Action: DY Business's 24/7 Self-Ordering Self-Service Platform

Understanding the Dynamic of DY Business

DY Business has revolutionized the way services are accessed and ordered with their innovative 24-hour self-ordering self-service platform. In a world that never stops moving, the ability to order services at any time of the day is a game-changer. This platform is not just a technological marvel but a testament to the company's commitment to customer convenience and efficiency.

By integrating cutting-edge technology and user-friendly interfaces, DY Business has created a seamless experience for its customers. The platform is designed to handle a wide range of services, ensuring that clients can access what they need, whenever they need it. This shift towards a self-service model is not just a trend but a necessity in today's fast-paced business environment.

The Benefits of 24-Hour Self-Ordering

One of the primary advantages of DY Business's 24-hour self-ordering platform is its flexibility. Customers no longer have to adhere to traditional business hours, allowing for more personalized and timely service. This means that whether you need a service in the middle of the night or on a weekend, the platform is there to cater to your needs.

Additionally, the self-service aspect of the platform significantly reduces the need for manual intervention. This not only speeds up the ordering process but also minimizes the chances of errors. With an intuitive interface and automated systems, users can place orders with ease, ensuring a smooth and efficient transaction every time.

From a business perspective, the 24-hour self-ordering feature also offers operational benefits. It allows DY Business to operate around the clock, maximizing their service availability and potentially increasing sales. This continuous service model can be particularly advantageous in industries where immediate service is crucial, such as emergency repair services or medical assistance.

The Future of Service Delivery

The implementation of a 24-hour self-ordering self-service platform by DY Business is a clear indication of the future of service delivery. As technology continues to advance, we can expect more businesses to adopt similar models, emphasizing convenience and efficiency for their customers.

Moreover, the success of such platforms will likely lead to further innovations in customer service. We may see the integration of artificial intelligence and machine learning to enhance the user experience, providing personalized recommendations and proactive customer support.

In conclusion, DY Business's 24-hour self-ordering self-service platform is not just a feature but a cornerstone of their business strategy. By embracing technology and prioritizing customer convenience, they have set a new standard in the service industry. As we move forward, it is likely that more businesses will follow suit, reshaping the way we interact with services in our daily lives.

盈利阶段性承压,盈利更优的海外收入占比提升

点评

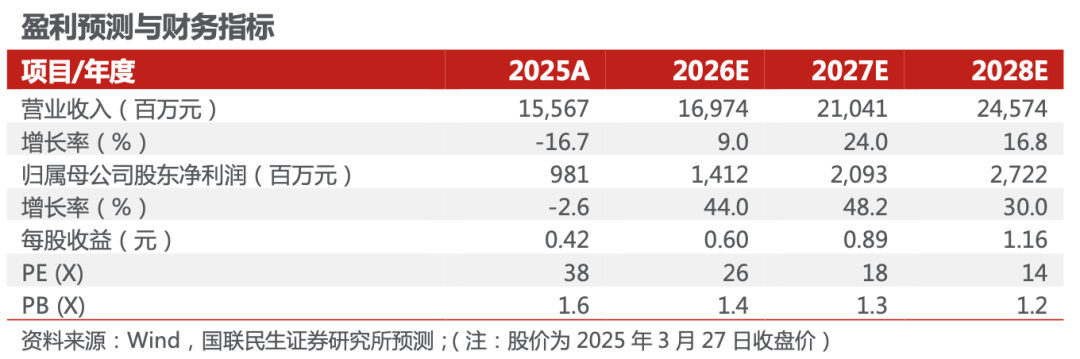

■ 事件:2026年3月26日,公司发布2025年年报。2025年公司实现营业收入155.67亿元,同比-16.68%;实现归母净利润9.81亿元,同比-2.59%;实现扣非净利润10.33亿元,同比+1.75%。2025Q4公司实现营业收入31.03亿元,同比-23.92%,环比-34.35%;实现归母净利润3.43亿元,同比扭亏为盈,环比-8.88%;实现扣非净利润4.07亿元,同比扭亏为盈,环比+2.09%

■ 行业供给阶段性过剩,盈利阶段性承压。2025年公司光伏玻璃销售量为11.87亿平米,同比下降8.16%,实现收入139.86亿元,同比下降16.83%;光伏玻璃业务毛利率为16.11%,同比提升0.47pct;2025年公司销售费用率8.03%,同比增加0.58pct。2025年,尽管新增产能投放节奏有所放缓,但前期积累的产能规模依然庞大,阶段性供需错配现象依然存在。受下游组件库存高企及排产调整影响,光伏玻璃企业库存压力增大,市场竞争加剧导致产品价格深度调整,受此影响,公司整体毛利率持续低迷。同时,由于行业供需失衡,为优化产能结构,公司部分窑炉进入冷修阶段,对公司的营业收入产生一定影响。尽管面临行业环境的巨大挑战,公司通过深化提质增效战略、优化运营管理机制等系列举措,仍未能完全对冲光伏玻璃价格持续探底带来的经营压力。

■ 盈利能力更优的海外市场收入占比提升。2025年,公司在亚洲其他地区、北美以及欧洲的销售收入分别为32.04、16.42、1.89亿元,分别同比提升3.08%、47.36%、16.11%,毛利率分别为23.23%、26.66%、21.34%,明显高于国内13.04%的毛利率。公司在盈利能力相对较高的海外市场销售收入增加,收入占比提升,有助于提升公司整体盈利能力。

■ 行业出清有望加速,公司有望受益于行业集中度提升。当前光伏玻璃价格持续低迷,行业盈利承压,市场调整周期加速优胜劣汰,缺乏成本优势、技术储备与规模效应的中小企业产能有望加速出清。随着部分落后产能的出清,市场供需关系呈逐步改善的态势,行业集中度有望快速提升。公司作为头部企业有望凭借资金实力、成本管理、规模优势、技术积累及客户资源优势,在行业整合中占据主动,有望进一步扩大市场份额,优化产能布局。

■ 投资建议:我们预计公司2026-2028年营收分别为169.74、210.41、245.74亿元,对应增速分别为9.0%、24.0%、16.8%;归母净利润分别为14.12、20.93、27.22亿元,对应增速分别为44.0%、48.2%、30.0%;2026-2028年EPS分别为0.60、0.89、1.16元,以3月27日收盘价为基准,对应2026-2028年PE为26X、18X、14X,公司是光伏玻璃的龙头企业,供需压力缓解后,盈利能力有望企稳回升,维持“推荐”评级。

■ 风险提示:下游需求不及预期,市场竞争加剧等。

公司财务报表数据预测汇总

研究报告信息

(601865.SH)2025年年报点评:盈利阶段性承压,盈利更优的海外收入占比提升

对外发布时间:2026年3月29日

报告撰写:

邓永康 SAC编号S0590525120002

朱碧野 SAC编号S0590525110045

王一如 SAC编号S0590525110041

林誉韬 SAC编号S0590525110044

电力设备新能源行业第一线最深度研究

期待与您的交流